Australian tax brackets change on 1 July 2026, and the change is simple: the rate on taxable income between $18,201 and $45,000 falls from 16% to 15%. Nothing else moves. The tax-free threshold stays at $18,200, the 30%, 37% and 45% brackets keep their current thresholds, and the Medicare levy generally applies on top at 2%, though reductions or exemptions apply in some circumstances.

If you earn $45,000 or more, the cut is worth up to $268 for the 2026-27 year. Here are the full brackets, what changed, and the part most people get wrong about how tax rates apply to their income.

The 2026-27 tax brackets (Australian residents)

For the 2026-27 income year (1 July 2026 to 30 June 2027), the resident income tax rates and brackets in Australia are:

| Taxable income | Tax rate (2026-27) |

| $0 – $18,200 | Nil |

| $18,201 – $45,000 | 15% |

| $45,001 – $135,000 | 30% |

| $135,001 – $190,000 | 37% |

| $190,001 and over | 45% |

The 2% Medicare levy applies on top for most taxpayers, and offsets such as the low income tax offset can reduce the final bill at lower incomes. Foreign residents and working holiday makers are subject to different tax rates and rules, and generally do not receive the tax-free threshold.

Compared with the 2025 tax brackets and the current 2025-26 year, the only line that moves is the second one: 16% becomes 15%.

What changed on 1 July 2026, and what’s still coming

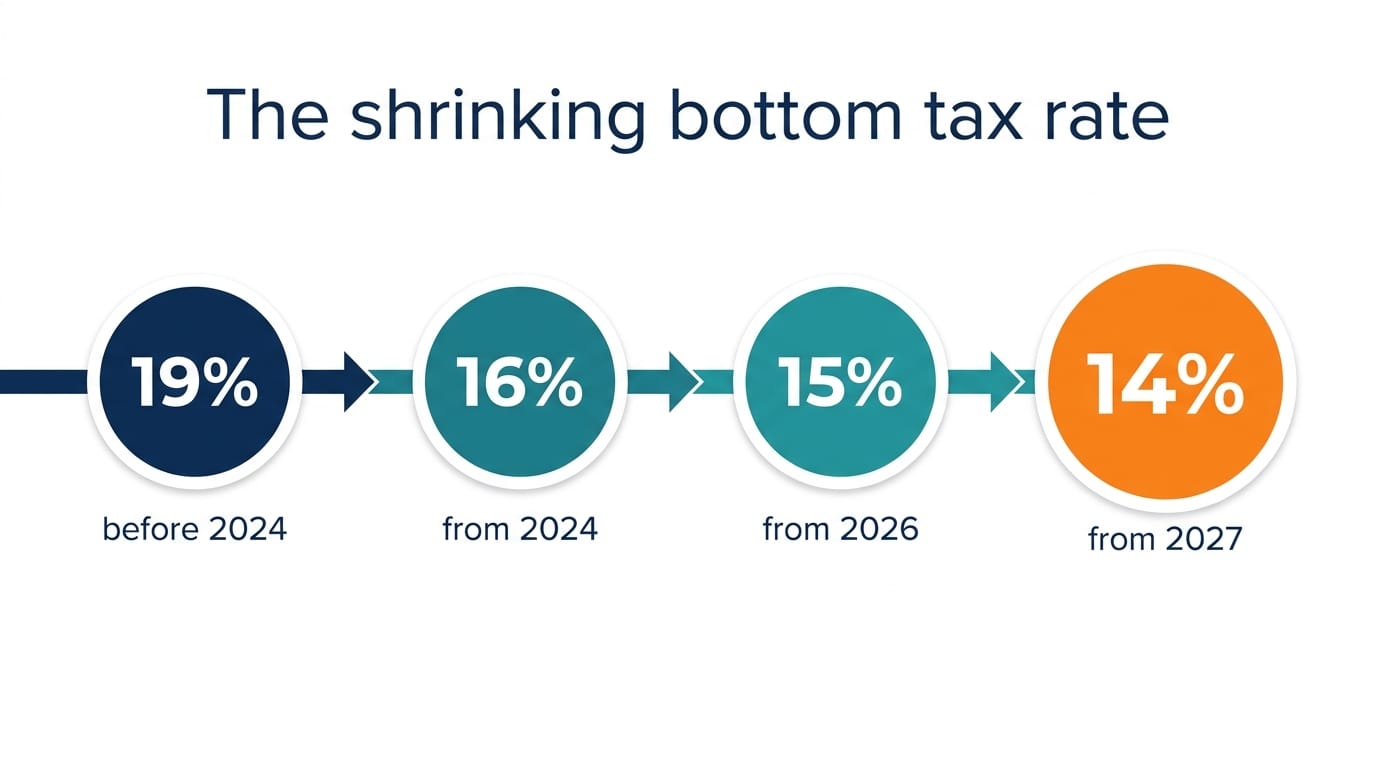

This is the second step in a series of legislated cuts to the bottom marginal rate. The stage 3 tax cuts that began on 1 July 2024 reduced the 19% rate to 16% and the 32.5% rate to 30%, and lifted the 37% threshold to $135,000. The 2025 federal budget then legislated two further reductions to that bottom rate: 16% to 15% from 1 July 2026, and 15% to 14% from 1 July 2027.

Because the band runs from $18,201 to $45,000, the maximum benefit of each 1% cut is $268 a year. Once the 14% rate arrives in 2027-28, the combined saving reaches roughly $536 a year against the 2025-26 settings. Modest, but automatic: PAYG withholding tables update from the first pay period starting on or after 1 July 2026, so take-home pay adjusts without you doing anything.

How tax brackets actually work on your income

The most persistent tax myth in Australia is that moving into a higher bracket taxes your whole income at the higher rate. It doesn’t. Australia’s tax rates are marginal: each rate applies only to the slice of income inside its band.

Take a salary of $100,000 in 2026-27. The first $18,200 is tax-free. The band from $18,201 to $45,000 is taxed at 15%, which is $4,020. The remaining $55,000 sits in the 30% band, adding $16,500. Income tax comes to $20,520, plus a $2,000 Medicare levy: about $22,520 all up, before any deductions or offsets. That’s an average rate near 22.5%, even though the marginal rate is 30%.

The practical takeaway: a pay rise can never leave you with less in your pocket because of tax brackets alone. Only the extra dollars are taxed at the higher rate.

Other changes landing on 1 July 2026

The bracket change isn’t travelling alone. From the 2026-27 year, a new standard deduction of up to $1,000 for eligible work-related expenses removes the need for itemised substantiation for taxpayers who choose that option; those with larger genuine claims can still itemise as usual. It first appears in returns lodged from July 2027, not in this year’s return.

Payday Super also begins on 1 July 2026, requiring employers to pay superannuation at the same time as wages rather than quarterly. For employees, it’s worth checking that contributions are arriving across all jobs. Additional tax on earnings attributable to very large super balances also applies from 1 July 2026. The rules generally affect individuals with total super balances above $3 million, with further provisions for balances above $10 million, and professional advice is worth obtaining because the calculation is complex.

There’s more to your tax than the brackets

If your income includes business profits, trust distributions or capital gains, the brackets are only the starting point. Where your income lands within them is the part you can plan with your accountant.

| General advice disclaimer |

| This article contains general information only and does not take into account your personal objectives, financial situation or needs. It is not tax, legal or financial advice. Before taking action, consider obtaining advice from a registered tax agent, accountant or suitably qualified adviser. |

Frequently Asked Questions

Do I need to do anything to get the new tax cut?

No. Employers apply updated PAYG withholding tables from the first pay period starting on or after 1 July 2026, so the cut flows into take-home pay automatically. Sole traders and others paying instalments will see it reconcile through their 2026-27 assessment. If your withholding looks off after July, ask your payroll team whether the new tables are loaded.

What were the tax brackets for 2025-26 by comparison?

Identical except for one rate: in 2025-26 the band from $18,201 to $45,000 is taxed at 16% rather than 15%. The thresholds of $18,200, $45,000, $135,000 and $190,000 are the same in both years, as are the 30%, 37% and 45% rates and the 2% Medicare levy.

Are more tax cuts already locked in after 2026-27?

Yes. The same legislation takes the bottom marginal rate from 15% to 14% on 1 July 2027, worth up to a further $268 a year. Beyond that, no further personal income tax rate reductions have been legislated. Other thresholds and tax measures may change through indexation or future federal budgets.

Does the $1,000 instant deduction replace my normal deductions?

No. From the 2026-27 year it gives you a choice: claim a flat $1,000 for work-related expenses without itemised substantiation, or itemise in full if your genuine claims exceed that. People with significant work expenses, rental properties or business income will usually still benefit from proper records and itemised claims.

Want to know what the 2026-27 brackets mean for your own numbers before 30 June? Book a free consultation with Crest Accountants on 07 5538 0999 or through our enquiry form.